Canada’s language training sector continued its recovery from the pandemic in 2023. A new annual report from Languages Canada, produced by industry research specialists BONARD, finds that Canadian language programmes – both English and French – enrolled a combined 112,564 students last year and delivered 1,234,447 student weeks of instruction.

That 2023 volume equates to 75% of pre-pandemic student numbers and 82% of pre-COVID student weeks. Just over nine in ten of those student weeks (92%) were for English-language learning, with the balance for French. Just over 80% of that total (83%) were delivered by private providers, with the remaining 17% delivered by language programmes operated by public institutions.

Students enrolled in English- and French-language training programmes in Canada, 2019–2023 (left); Student weeks delivered by English and French language training providers in Canada, 2019–2023 (right). Source: BONARD/Languages Canada

Nearly two-thirds (63%) of all student weeks were delivered via in-person instruction in 2023, with another 30% given online (whether for students in Canada or abroad). The final 6% of student weeks relied on a hybrid delivery model.

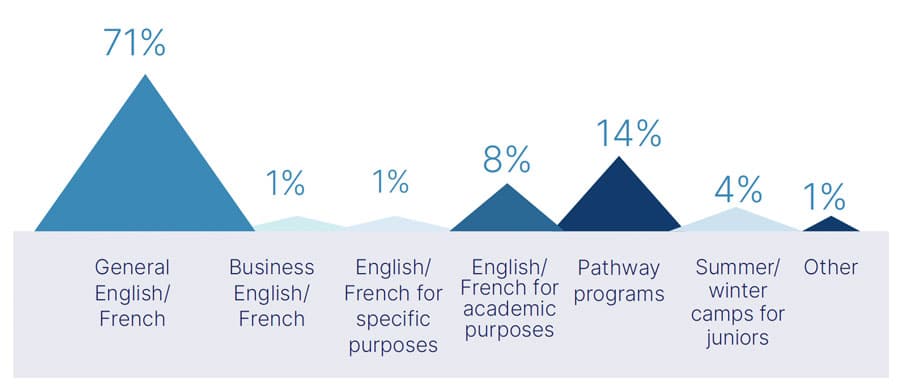

As we see in the outline below, the majority of students were enrolled in general language studies, pathway programmes, or academic preparation courses.

Enrolments in language studies in Canada, by course type, for 2023. Source: BONARD/Languages Canada

Where do students come from?

More than three in four languages students in Canada (76%) come from either Asia or Latin America. The following infographic highlights the top ten sending markets for 2023. All of those top sending countries recorded year-over-year growth in 2023, with the exception of Colombia, which declined by -6%.

Top ten sending markets for Canadian language-learning programmes, 2023. Source: BONARD/Languages Canada

Visa status and visa challenges

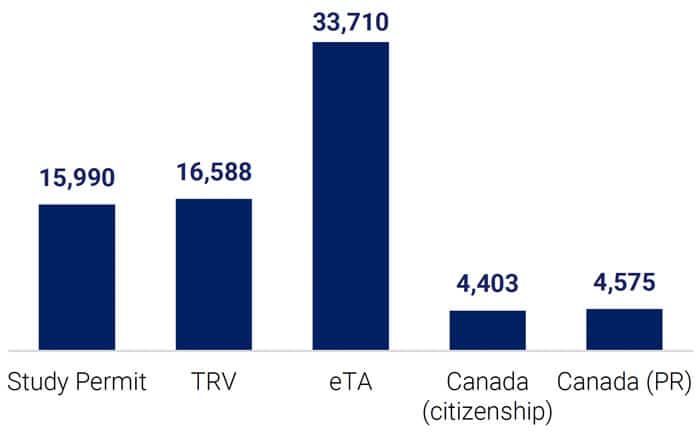

The following chart indicates that many students attended a Canadian language programme with a visitor visa (“eTA” or electronic travel authorization in the legend below). But significant numbers also travelled to Canada under a study permit or temporary resident visa.

Student numbers by visa type, 2023. Source: BONARD/Languages Canada

The report adds that, “In 2023, the fastest-growing visa category was the Temporary Resident Visa (TRV). The number of students entering Canada through the TRV route increased from 8,559 in 2022 to 16,588 in 2023, surpassing pre-pandemic levels. This also caused a drop in the average course duration seen predominantly in the private sector. On the other hand, the number of students on study permits decreased from 17,191 in 2022 to 15,990 in 2023 due to issues with visa processing and refusals.”

Join 37,000 subscribers

and stay up to date on International Recruitment

As we have seen in other destinations this year, however, Canadian language schools report that visa issues prevented thousands more students from pursuing their studies in 2023. The report estimates that at least 2,671 students were not able to travel to Canada as planned due to processing delays for temporary resident visas, and that a further 4,479 students were not able to travel due to study permit delays.

This means that visa processing issues disrupted the travel plans for a minimum of 7,150 language students in 2023 – a number equivalent to 7% of the total enrolment for the year. Commenting in a foreword to the report, Languages Canada Executive Director Gonzalo Peralta said, “In 2019, Canada’s language programmes generated CDN$6.7 billion and 75,000 jobs, mostly derived from export revenues. In 2023, that figure decreased to CDN$5.5 billion and 62,000 jobs. This drop was not due to lack of opportunity, promotional efforts, or support from some areas of government, but was primarily due to immigration policy.”

The volume of Chinese students choosing to study abroad is rising and may even return to pre-pandemic levels in the next year, according to industry experts and data trends. But the nature of demand is changing due to the increasingly complex nature of this crucial sending market. While rankings and prestige still matter greatly to many Chinese students, other factors have risen in importance, including:

Proximity and safety, which became top drivers of Chinese families’ choice of destination in the pandemic and which remain major priorities;

Cost, in a context of high job insecurity in China and a faltering post-pandemic economic recovery;

Employability outcomes, as youth unemployment remains a key problem in China.

Three of the “Big Four” English-speaking destinations (Australia, the UK, and US) remain the most preferred options for study abroad and are the largest hosts of Chinese students:

US: 289,530 (2022/23, 0% growth y-o-y)

Australia: 166,420 (2023, +6.5% growth y-oy)

UK: 151,675 (2021/22, +56% growth y-o-y)

But Asian destinations – especially Japan – as well as Singapore, Hong Kong, Malaysia, and Thailand now command significant share of interest due to advantages such as proximity, affordability, and the presence of many highly ranked universities.

Asian destinations’ advantages shine even brighter in a year in which Australia, Canada, and the UK have more restrictive policies around international students – and leading into the November 2024 US presidential election. As it stands, former president Trump (whose platform is heavily premised on limiting immigration) has a very good chance of being elected for the second time. Recent research has found this prospect to be appealing, or at least a neutral proposition, for some prospective international students, but China/US tensions rose when Trump was president and families of prospective Chinese students will no doubt be aware of this.

Canada used to enrol many more Chinese students than it does now; enrolments are down about 40,000 since 2019. In 2023, Japan enrolled more Chinese students (115,495, +11% over 2022) than Canada did (101,150, +1% over 2022).

South Korea (68,065 in 2023, +6.5% y-o-y), Germany (42,580 in 2022/23, +9%) and Malaysia (39,010 in 2022) also host significant numbers of Chinese students. In 2023, Chinese applications to Malaysian institutions were up 21% compared with 2022 (to 26,630), and they have doubled since 2019.

Thailand is very popular among Chinese students looking for affordable education, and the number of Chinese students studying in Thailand has doubled within the past five years to over 20,000.

Join 37,000 subscribers

and stay up to date on International Recruitment

Otherwise, The China Daily reports that “Russia, Belarus, Italy, Ukraine, Ireland, Spain, Sweden and Switzerland have made it to the list of top 20 overseas education destinations for Chinese students.”

The ups and downs of destinations’ popularity

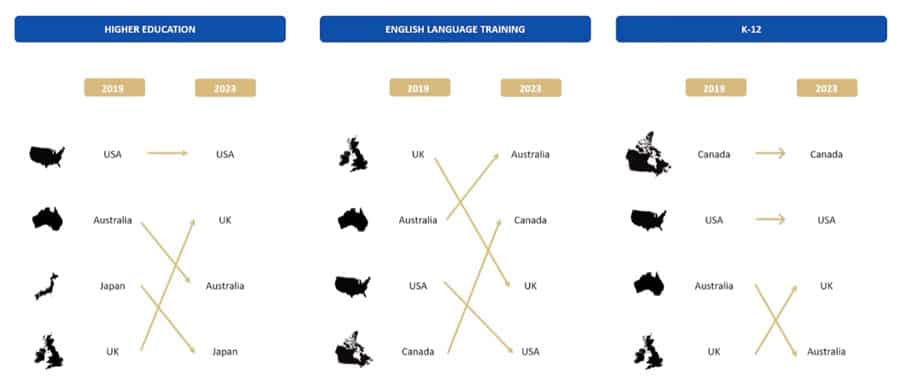

Viewers of a recent webinar hosted by international education industry research firm BONARD, Recruiting students from China, were presented with data showing that for Chinese students looking for university degrees, the UK has become much more popular in the past few years. In fact, UK universities are hosting more Chinese students now than in 2019. This means that the UK is the only destination other than Hong Kong to have exceeded its pre-pandemic volume of Chinese students. The US and Australia have recovered about 78% of their 2019 volume, while Canada has recovered 72%.

Chinese enrolments have grown in the UK since the pandemic. Source: HESA

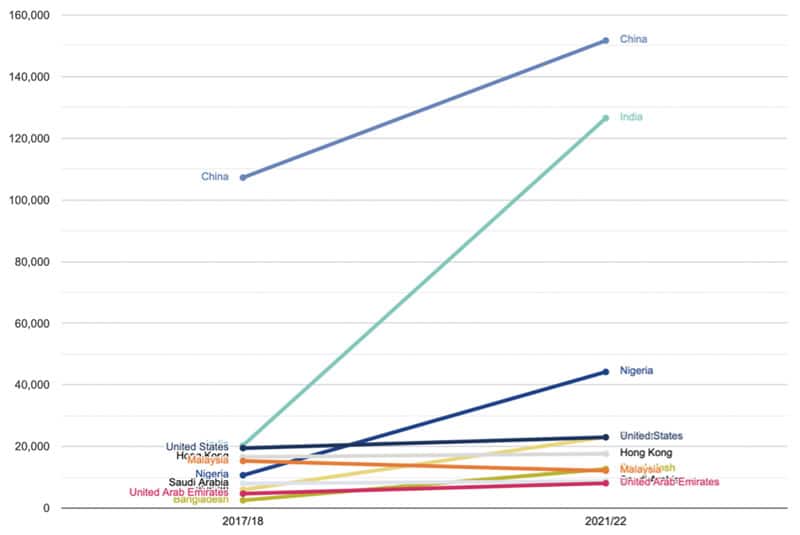

The US has held its ground in terms of its popularity among families of prospective Chinese students according to the BONARD graphic below, while Australia and Japan have lost some traction in the market. Canada is not even in the top four in 2023 for Chinese higher education students.

Chinese students’ destination preferences, by sector, 2023 versus 2019. Source: BONARD

When we look at English-language training, however, it’s Australia and Canada that have gained students’ interest, while the UK has dropped to third. The Australian ELICOS sector’s increased share of demand may be short-lived, however, as visa rejection rates for Chinese English-language students have increased over the past year. While 97% of Chinese applications for Australian universities were approved as of June 2024, only 56% of Chinese ELICOS applicants receive a positive response to their visa application.

Sociologist Angela Lehmann, chair of the Foundation for Australian Studies in China, told Times Higher Education that in some Chinese circles, Australia’s more restrictive visa policies are being seen as “anti-China policy.” Declines in Chinese students in ELICOS could also have a debilitating effect down the line for Australia’s universities, as the higher education system relies to a significant degree on recruiting international students from ELICOS.

For families of K-12 students, Canada is the leader, as it was in 2019.

Chinese outbound set to surge – where will students go?

Speaking during the BONARD webinar, Mingze Sang, president of the Chinese agency association BOSSA, said the Chinese outbound student market recovered to about 80% in 2023, and he expected as many Chinese students will choose to study abroad in 2024 as before the pandemic. When polled, 13% of webinar attendees said they expected a major increase in Chinese student numbers in 2024 compared with 2023, 30% expected there will be more Chinese students, 34% expected stability in numbers, and 16% expected fewer Chinese students.

The UK is the only destination of the Big Four that has maintained its position – appeal-wise and in terms of enrolments – in the Chinese market. But even there, dynamics have changed: Mark Corver, managing director of data and analytics at the consultancy dataHE, says that lower-ranked UK universities are less able to compete in China than they once were – not least because elite UK universities are recruiting in China more aggressively than in the past, and also because there are a growing number of highly-ranked universities in Asia.

Elite US universities are having no issues maintaining Chinese enrolments – but other US institutions are facing a more price-sensitive student consumer in China, which is making it more difficult for many to recruit in the market. Writing in Inside Higher Ed, Xiaofeng Wan explained that there is a misconception about the ease with which Chinese families self-fund their children’s education abroad. The institution he works at, Amherst College, surveyed Chinese parents “to gain a deeper understanding of the current thinking among Chinese families on affording an American education.”

Mr Wan noted that of the 343 Chinese parents Amherst surveyed in in late June 2024, 90% intended to fully fund their children’s education in the US. But there is more to this story: many of those parents will be stretching their savings to afford their children’s education, and many could use scholarships/aid to be less pressured financially. Of the parents Amherst surveyed:

35% had an annual after-tax income between US$74,740 and US$149,481;

30% took home US$14,948 to US$74,739;

2% had an after-tax income below US$14,948.

That middle bracket – the 30% with annual after-tax income of US$14,948 to US$74,739 – will obviously find it challenging to afford a four-year American college programme. The 2% with incomes below US$15,000 will find it even more difficult.

But Chinese parents tend not to apply for aid because they believe it will reduce their children’s chances of admission. Mr Wan said their concerns are valid:

“There are only seven colleges in the United States that adopt a need-blind admission policy for both domestic and international applicants and that truly do not consider an international applicant’s ability to pay during the admission process— namely, Amherst, Bowdoin and Dartmouth Colleges; Harvard, Princeton and Yale Universities; and the Massachusetts Institute of Technology.”

All this brings us back to the question of where Chinese students will go in the next couple of years for study abroad. If they can’t afford the UK or US, they may not choose Australia or Canada given policy changes in those countries and Canada’s generally declining appeal for Chinese families looking at higher education options abroad. (Study permits for Chinese students applying to Canadian institutions fell by 40% between 2018 and 2023).

Some observers have begun to parse the market by generation, where older generations remain strongly drawn to the Big Four destinations, and younger cohorts are much more interested in regional study destinations within Asia. That trend towards regional study seems to have been accelerated by the pandemic as greater numbers of Chinese students gained more experience with study destinations closer to home within Asia during those years.

Japan, Malaysia, Taiwan, and South Korea have all set ambitious new international enrolment targets, and there is no doubt their universities and schools are recruiting heavily in China right now. China is by far the top international student segment for Japan, Taiwan, Malaysia, Thailand, and South Korea.

Chinese more open to a range of destinations

Chinese students are not only becoming more interested in staying in Asia, but they are also open to whatever destination/institution best meets their needs – whether that’s through attractive pricing, cost-of-living, programmes, or, increasingly, internships.

Chinese youth unemployment rose dramatically through, and after, the pandemic, in tandem with slowing growth in China’s economy. The youth unemployment rate rose above 20% in June 2023, and soon after, the Chinese government suspended public reporting of this employment metric. Suffice to say that jobs are very much on the mind of Chinese students and families when they choose where to study. Su Su, senior project consultant at BONARD’s China branch, said in the BONARD Recruiting students from China webinar that:

“The so-called Return-On-Investment is a term I hear mentioned more and more by parents and students when planning overseas studies. Parents will consider affordability and employability when choosing a school and will appreciate internship opportunities in local companies.”

In 2021, a BOSSA survey of around 8,000 Chinese students found that nearly 30% of students said they would increase the number of countries they were applying to to ensure the stability of their study abroad plans. And China Institute of College Admission Counseling’s (China ICAC) 2023 Annual Report found that “58% of schools reported that over half of their students applied to colleges in multiple countries.”

Regional targeting is a must

Su Su said it’s imperative for institutions – wherever they are – to understand that Chinese families are strongly influenced by schools who spend the money to send a representative to where they live in China. She provided the example of a K-12 school in Switzerland that sent a representative to Zhengzhou (North China) to develop a strong rapport with parents there, and noted that within the span of 2 years, not only the school but also the destination of Switzerland became incredibly popular in Zhengzhou.

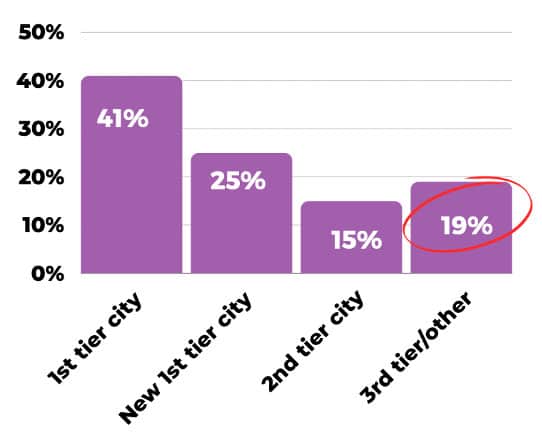

Ms Su used the Swiss school example to impress the importance of precise market targeting in China. It’s a huge country, and different programmes and destinations are more or less popular in certain regions, and lower “tier” cities hold great potential. (There are four city tiers in China based generally on economic prosperity: Tier I, New Tier I, Tier II, and Tier III.)

Edufair China notes:

“Tier I cities are saturated with recruitment from schools with well-established market footholds. Recruiting in second and third-tier cities means less competition from other foreign institutions for both agents and students. The further schools move from first-tier cities and markets, the more likely they’ll be to find students and agents eager to engage.”

Similarly, the survey informing China ICAC’s 2023 Annual Report secured participation from significantly more institutions in Tier III cities – “growing from 8% last year to 19% this year … indicating a growing interest and engagement [in international education] from a broader range of regions.” Overall, 111 institutions across China participated in the survey.

More than a third of high schools participating in China ICAC’s 2023 survey are located in Tier II or III cities. Source: China ICAC

What’s more, lower-tier cities also hold the majority of China’s international schools, which offer excellent recruitment opportunities for foreign educators. Sunrise Education notes in its Trends in International Education and Student Mobility in 2024 report:

“Regionally, Tier 2 and 3 cities are home to 62.1% of China’s international schools. Tier 1 cities Beijing and Shanghai account for 11.2% and 11.9% respectively. Guangdong, which includes two Tier 1 cities as well as many Tier 2+ cities, accounted for 14.8%.”

In 2024, these are the cities categorised into four tiers (Tier I, New Tier I, Tier II, Tier III), as explained by Siam Commercial Bank (Thailand):

“First-tier cities comprising Beijing, Shanghai, Guangzhou, and Shenzhen. Those are the most 4 developed cities in economics and infrastructures as people have high purchasing power. All are large cities that have political and cultural influence over the country.

New first-tier cities comprising 15 cities; Chengdu, Hangzhou, Chongqing, Wuhan, Xi’an, Suzhou, Tianjin, Nanjing, Changsha, Zhengzhou, Dongguan, Qingdao, Shenyang, Hefei, and Foshan. All are big cities with high development in economics and infrastructures after the 4 First-tier cities. Consumers also have high purchasing power.

Tier 2 cities comprising 30 cities and most are major county or on the east coast; Xiamen, Fuzhou, Wuxi, Kunming, Harbin, Jinan, Changchun, Wenzhou, Shijiazhuang, and Nanning, etc. All cities are not as booming as the new First-tier cities.

Tier 3 cities comprising 63-71 cities (depending on the ranking person) which are as prosperous as the district level and are considered economically developed cities.”

Digital marketing tips

In China more than any source country, adapting digital marketing to the local market is key – on search platforms such as Baidu (aka “China’s Google”), which has a 70% share of the “traditional” search engine market, and on social media giant WeChat (estimated reach of over 1.3 billion monthly active users). In addition to Baidu, Sunrise Education says that using alternate discovery platforms in addition, such as Zhihu and Toutiao, can add a boost to marketing. You can check out Sunrise Education’s 2024 Trends in China’s Digital Landscape whitepaper here for more information.

Sekkei Digital Group advises:

“Transitioning or building your site means more than just simply translating it into Chinese. Your content will need to be equipped to cater to Chinese online habits. You can achieve this by considering website layout preferences, image preferences, and design choices. Localizing your site[2] will also improve its SEO ranking because most search engines in China favor a “.CN” domain name over foreign web pages. Through this, international applicants and other Chinese users can find your website easier when they look for international schools or exchange programmes.

On top of tailoring your website to the Chinese market standards and appearing on top of search engine results, remember that you need reputable web hosting services in China and an ICP licence.”

Sunrise Education says short-form videos remain exceptionally popular in China:

“Short-form video accounts are a useful new tool for recruitment in China. Douyin offers a robust advertiser backend, and Bilibili offers an opportunity to build an organic following as well as to run targeted digital campaigns. Douyin grew from a niche platform before the pandemic to having more than 731 million monthly active users (MAU) in 2022, while Bilibili has reached 341 million MAU. These platforms saw meteoric growth during the pandemic, but they’ve demonstrated staying power and reflect the broader global shift to short-form video like we’ve seen in the west with TikTok and Instagram Reels.”

Working harder is a must, and career supports are key

The British Council’s senior lead for culture and education, Joshua Gabriel, a panelist on the BONARD webinar Recruiting students from China, said:

“Parents and students are going to be looking more at employment outcomes and return on investment from study abroad, so employability is going to be a key push in 2024. Students are applying to multiple institutions, which means students have more choices. The appetite remains strong from China, but institutions around the world may need to work harder.”

Rona Wu, manager of ShinyWay International, concurred that employability is a major driver in 2024, saying that finding a job is a huge stress for Chinese students. BOSSA’s president Mingze Sang said that all educators need to realise that families are most concerned about jobs for their children, and career supports must be built into programmes if institutions want to be competitive in the Chinese market.

As for whether Asian destinations’ new popularity will prove a serious challenge for Western institutions recruiting in China, Mr Sang reminded the audience that destinations such as Singapore and Hong Kong are small and limited in terms of capacity. In this sense, their popularity may not have a profound effect in terms of share of the Chinese market.

Top Chinese students, however, are paying particular attention to the most highly ranked Asian institutions. Mr Gabriel pointed out that Hong Kong and Macao are attractive especially for their combination of high-quality education and safety.

Ms Wu says that a common tendency is for Chinese students to apply to a Western and an Asian institution, say in the UK and in Hong Kong, and then to compare their offers. Which is more highly ranked? Which is more affordable? Which offers internships?

In essence, Chinese students now know they have more choices, and their new habit of applying to institutions in multiple destinations is one worth keeping in mind as educators sharpen their recruiting strategies this year. The market still holds great opportunities, but it will take more to convince students that an institution is the best fit for them.

Chukwuemeka Odumegwu Ojukwu University (COOU), Igbariam, Anambra State has unveiled a five-year Tree Planting/Climate Action Plan towards combating the challenges of climate change in Nigeria.

The COOU Ag. Vice Chancellor, Prof Kate Azuka Omenugha told participants at a one-day 2024 Climate Action Summit, held at the University’,s ETF Auditorium on Wednesday, that the roadmap was geared toward achieving the ultimate goal of a zero-carbon Varsity in Nigeria.

Omenugha said that the climate change policy and action plan encapsulated the state’s vision for combating the challenge of climate change and achieving the ultimate goal of a zero-carbon Anambra State.

She also set up students environmental task force in the Institution as part of her action plan against the challenges.

According to her, the Ojukwu University has successfully updated the action plan to reflect governor Chukwuma Charles Soludo’s vision of making Anambra a clean, green, livable and prosperous state in Nigeria.

In her words, “I am delighted to let you know that Chukwuemeka Odumegwu Ojukwu University (formerly Anambra State University), is the first University in Nigeria to have developed a Climate Action Plan to help achieve an emission-neutral institution by 2029.

The emergence of this action plan establishes our University’ as the greener University in the country.

“Our appreciation goes to the Anambra State Ministry of Envirmement, Nigeria Conservative Foundation (NCF), Nigeria Meteorological Agency (NiMet), National Council of Climate Change, AI/Climate Action Future, Green Envirmement/Climate Change Initiative and the Nigerian Institute of Public Relations! (NIPR) which the University has reached an agreement, and which has also helped us update our Climate Action Plan in line with prevailing realities in the University.

“This maiden edition gave us an opportunity to present the new University Climate Action Plan to the World.

“Our objective now is to carry out this awareness to the entire University community to get the staff and students to imbibe the culture of climate awareness in their homes and lifestyles, the VC noted.

The State Governor, Chukwuma Soludo in his brief speech while declaring the summit open, urged residents in the state to support every necessary action towards protecting the environment.

Governor Soludo was represented at the summit by his Chief of Staff, Mr Ernest Ezeajughi.

The keynote speaker of the Summit and the Director General of Nigeria Conservative Foundation (NCF), Dr. Joseph Onoja while delivering his speech, on the theme, “Tree-Mendous Strategy For A Sustainable Future”, congratulated the University management on the unveiling of the ,5-years Tree Planting/Climate Action Plan, noting that the effects of environmental problems knew no borders.

The DG encouraged government, communities and individuals to actively participate in the tree planting project for forest reservation.

He expressed the Foundation’s readiness to partner the University in combating the challenges.

The event was also attended by the Nigerian Former Ambassador to Spain, Amb. Bianca Ojukwu, Chairman of the University Governing Council, Prof. Chidi Odinkalu, Member of the University Governing Council, His Royal Highness, Igwe Dr. Oranu Chris Chidume, His Royal Highness, Igwe Alex Onyido, Chief Okeke Ogene (National Vice President, Ohaneze Ndigbo Worldwide), Chairman of the occasion, Mr Peter Nwosu, Prof. Kingsley Nwozor, Managing Director and Chief Executive Officer of Anambra State ICT Agency, Mr Chukwuemeka Fred Agbata, the unveiler/Managing Director of Kacel Oil and gas, Izuchukwu Ifemelumma, Mrs. Chiamaka Nnake (Commissioner for Economic Planning), Mr. Christian Udechukwu (Commissioner for Industry), Barr. Ifeanya Anthony ( Commissioner for Petroleum), Commissioner for Envirmement, Engr Felix Odimegwu, Commissioner for Culture and Entertainment, Comrade Don Onyeji, Prof. Phil Eze-Phil (ANSEWCCA), Former MD/CEO ABS Dr Uche Nworah and Ms. Chinwe Okoli (SPAD on Innovation and Business Incubation), amongst others.

The Paradise News gathered that the summit also feature panel discussion, displace of traditional dance and the commencement of the 1 million tree planting project.

An updated analysis from Global Affairs Canada (GAC) estimates that the combined direct and indirect GDP contribution of all students expenditures in the country amounted to CDN$30.9 billion (US$23 billion) in 2022.

Education exports, as measured by the total value of international students in Canada (CDN$37.3 billion in 2022), accounted for just over 23% of Canada’s total service exports in that year, and 1.2% of Canada’s GDP overall. The report adds that, “In 2022, the total amount of international student spending (CDN$37.3 billion) surpassed the value of Canada’s exports in many product categories, for example, wood and wood products (CDN$25.7 billion), fertilizers (CDN$17.9 billion), or electrical or electronic machinery and equipment (CDN$19.2 billion). Total international student spending in 2022 was equivalent to about 4.8% of the total value of Canada’s merchandise exports.”

Also for 2022, international student spending is estimated to support 361,230 jobs in Canada, or 246,310 FTE positions.

“Over the past two decades, the number of study permit holders in Canada increased more than sixfold, with every province and territory recording positive gains,” notes the report. “Although Ontario attracted the greatest number of international students, it is worth noting that Prince Edward Island recorded the highest percentage increase in the number of study permit holders – from 2000 to 2022, the percentage increase has been over 1,800%.” Ontario hosted just over half of all international students in the country (51%) in 2022. British Columbia accounted for nearly a quarter (22%), and Quebec another 12%.

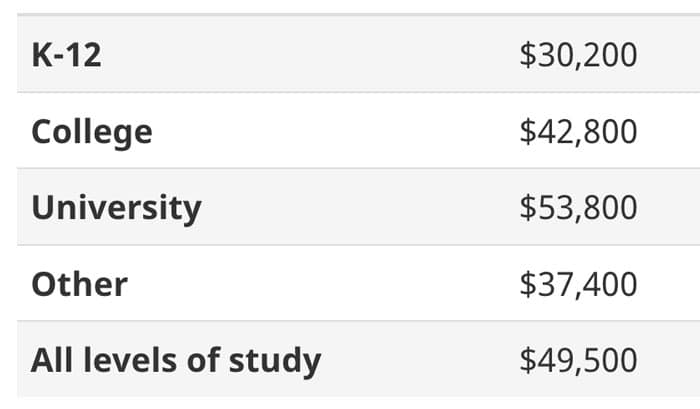

The GAC analysis attributes roughly 97% of that economic impact to long-term students – that is, students enrolled in programmes of six months or more. The following table breaks that long-term-student spending down into per-student averages for various levels of study.

Average annual per-student expenditures – cost of education and cost of living – for long-term international students, 2022. Source: Global Affairs Canada

Not surprisingly, GAC finds that India has been the big driver of that recent-year growth: “Detailed data indicates that of the top source countries for long-term students, the biggest increase was from India (+47%, with 319,130 study permit holders in 2022)…Other top source countries for long-term international students that experienced strong increase between 2021 and 2022 include:

Philippines (+112% to 32,455)

Hong Kong (+73% to 13,100)

Nigeria (+60% to 21,660)

Colombia (+54% to 12,440)”

The other significant feature that comes through in the GAC estimates is just how quickly the economic impact of international students has expanded over the past decade. Overall student spending more than doubled between 2016 and 2022 alone, from CDN$15.5 billion to CDN$37.3 billion, for an average annual increase of nearly 16% per year.

Join 37,000 subscribers

and stay up to date on International Recruitment

That pattern would have certainly continued in 2023, a year after the period of the current GAC analysis, when foreign enrolment in Canada climbed by 29% year-over-year. Even a crude extrapolation of the GAC figures from the year before would suggest that international students’ contribution to Canadian GDP would have approached CDN$40 billion (US$30 billion) in 2023.

A new report from English UK draws on survey responses from 91 member centres to conclude that many ELT schools in the country found it necessary to limit enrolment in 2023 because of a shortage of suitable student housing.

Responding ELT providers cumulatively reported a shortage of more than 6,600 beds last year, a shortage which led many to constrain student numbers.

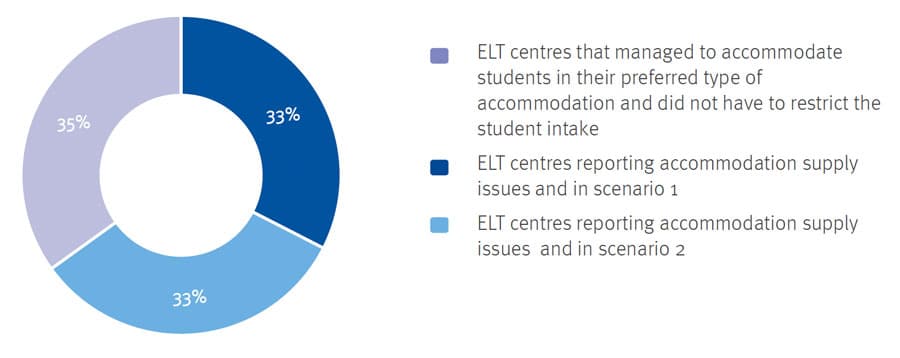

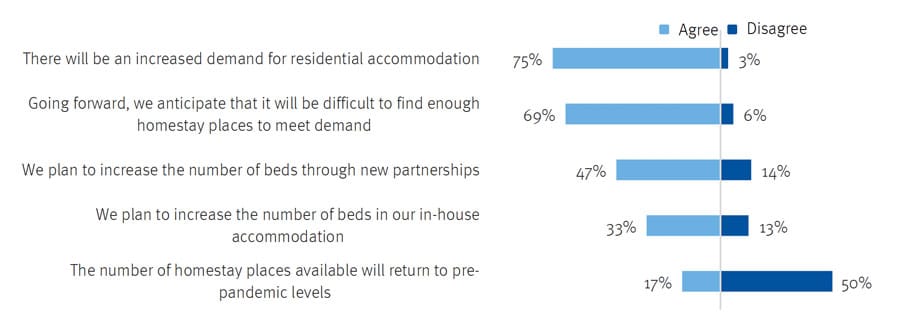

The following chart provides a high-level breakdown of the scale of housing challenge for reporting ELT centres. It illustrates that just over a third (35%) did not have to restrict their student intakes due to housing. Nearly two-thirds, however, did report significant housing impacts. The “scenario 1” referred to in the chart describes “ELT centres that managed to place all their students in their preferred type of accommodation type because they restricted the 2023 student intake”. Meanwhile, “scenario 2” refers to centres that “restricted the size of student intake in 2023 and still did not manage to place all their students in their preferred type of accommodation.”

In other words, two-thirds of the responding ELT schools found it necessary to limit their student intakes in 2023 due to housing constraints.

UK ELT centres reported housing constraints and student intake limits for 2023. Source: English UK

The report concludes that, “Totalling the figures from scenarios 1 and 2, cumulatively, 66% of the respondents reported accommodation shortages. These respondents could have used over 6,600 additional beds: 3,815 in residences and 3,358 in homestay places…This means that, potentially, 6,600 more students could have been enrolled by these UK ELT centres in 2023.”

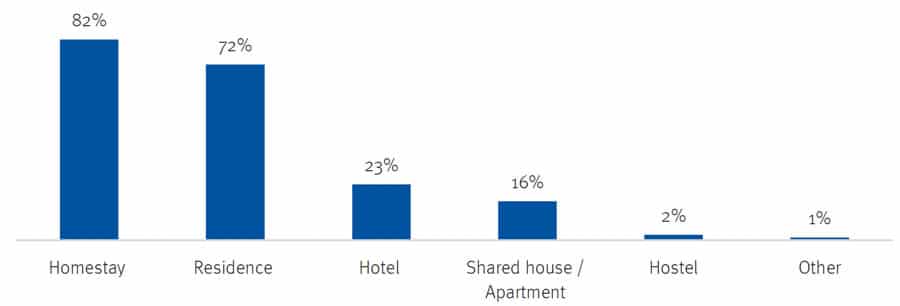

The additional chart below outlines the main types of housing offered by providers within the sector, with most relying on homestay (82%) and residence (72%) options.

Accommodation options offered by UK ELT centres in 2023. Source: English UK

Nearly half (42%) of responding centres indicated in the survey that they were working to increase the number of beds available to their students for summer 2024, but, as we see in the next chart below, there is broad consensus around some of the important housing issues facing the sector when it comes to student housing.

Join 37,000 subscribers

and stay up to date on International Recruitment

Accommodation trends anticipated by UK ELT centres. Source: English UK

The report concludes that national advocacy campaigns to recruit additional homestay families, and expanded partnerships between schools and local housing providers or institutions, will be key steps to ease the housing challenge for the sector going forward.

“A lack of suitable student accommodation impacts every stakeholder in the international education sector: it can jeopardise the student experience, hinder recruitment efforts, and ultimately damage the reputation of a study destination,” adds the report, which can be commended for the concrete evidence it provides as to how housing constraints directly impact recruitment and student intake.

In January 2024, Canada announced a two-year cap on international enrolments. That cap was mandated by the federal government, with an allocation of student visa applications distributed to provincial and territorial governments and from there on to individual institutions and schools.

Australia has announced a cap of its own, the implementation of which is currently planned for January 2025, and it too is expected to be centrally set and managed by government.

Under pressure from their own national government, Dutch higher education leaders announced a plan in February 2024 to voluntarily limit international student intakes.

Those examples all arise from the same context and political imperative, which is simply to limit inbound migration, including the flow of international students. That pressure to cap or reduce student numbers arises from a variety of factors, including broad inflationary pressures, rising costs of living, economic uncertainty, and housing shortages.

However, the merits of any such cap – whether one should exist at all; how it should be designed and managed – can be hotly debated. And indeed that conversation is continuing in destinations around the world throughout this year.

Within the broad question of capping enrolment for a given study destination, or even a given institution, lies another important issue which is specifically relevant for post-secondary institutions that enrol both domestic and international students: what is the optimal balance of domestic and international enrolment?

The question is complicated and naturally resists a “one size fits all” answer, in part because the “right” proportion of foreign students will vary by factors such as level of study (college versus undergraduate versus graduate or post-graduate, in particular), and also by institutional setting (urban versus rural or regional) and the extent of the institution’s research portfolio.

Join 37,000 subscribers

and stay up to date on International Recruitment

This is a live issue in Australia currently, for example, where consultations are ongoing around a planned enrolment cap. Last month, Deakin University Vice-Chancellor Iain Martin argued for an alternative to a government-mandated cap. In an echo of the earlier Dutch example, Professor Martin proposed a blanket cap of 35% – that is, that each Australian university would voluntarily hold its foreign student numbers below a benchmark of 35% of total enrolment. He further suggested that no more than 50% of the foreign enrolment at a given institution should come from any one country, and that there should be no more than 40% of foreign students in any one faculty or field of study within the university.

“If we get [the government-led cap implementation] wrong it will have profound and lasting impacts,” he said, speaking to The Australian. “The government has to realise [international student flow] is not something you can switch on and off at will.”

In a similar vein, in a recent interview with The Guardian, Alec Cameron, the vice-chancellor of RMIT University, argued that international students should not account for more than a third of the total enrolment at a given university. “I wouldn’t [allow universities] to go above one-third,” he said. “Otherwise, the community forms a view about universities.”

Enrolment caps – self-imposed or otherwise – that run anywhere in that 33-35% range are noteworthy because many institutions will already have foreign enrolments above that level. Nearly half (47%) of the enrolment at the University of Sydney, for example, is made up of international students. And that proportion ranges above 35% at some of the country’s other leading research-intensive universities, including the University of Melbourne, the Australian National University, the University of Queensland and the University of Adelaide.

The Group of Eight (Go8) is a peak body representing all of those research universities. In its recent consultation submission to government, it argued, “The central command and control regime for international education that caps represent simply will not work. International students have too many quality options in a global context and will not be reallocated around Australia at the whim of the Government.” Responding to Professor Martin’s suggestion of a blanket 35% cap, Go8 Chief Executive Vicki Thomson said that such an approach is too “blunt and does not take into account different contexts, for example the mix of undergraduate and postgraduate.”

Meanwhile in Canada

Keep that 33-35% threshold from the Australian example in mind, because it was reflected again recently in a completely different setting. British Columbia, or BC, is Canada’s westernmost province and home to about a quarter of all foreign students in Canada.

The provincial government in BC is reportedly considering an approach where public, post-secondary institutions would be required to hold international student numbers to no more than 30% of total enrolment. Strictly based on recent headcount data from the BC Ministry of Post-Secondary Education and Future Skills, foreign enrolment at most public colleges, institutes, and universities in the province would fall below that threshold currently, but certainly there are some that are bumping up against that line, or perhaps over it.

Building the formula

All that to say there is no easy answer to the question of what is that right mix of foreign and domestic enrolment. Institutions that emphasise post-graduate programmes and/or have extensive research portfolios may naturally attract international scholars in larger numbers. Indeed, they may also need those international cohorts to help offset gaps in research funding or other structural financial issues.

At the same time, there is the question of social or community license for international education. That is, the extent to which local or national populations welcome and support international students during their studies. That social license can be sorely tested in times of economic struggle or in the face of a housing crisis such as we are seeing in many countries this year.

Keep in mind as well that every university and college has to be concerned about the broader social license under which it operates: the community support for post-secondary education and the extent to which it is perceived as a public good. We see that reality reflected in comments such as Professor Cameron’s, where he muses about the community view of universities, and it is a real consideration for any institution in terms of its relationships with governments, community leaders, and other key stakeholders.

Finding the “right” proportion of international students is as much about holding all of those important considerations in balance as anything else. There probably is no absolute answer to the question, but it is interesting to see even in these few examples the threshold settling in that 30-35% range. Pushing the benchmark much below that would trigger significant impacts for institutions in most leading destinations. Setting it much higher would, intuitively at least, start to press on that social license more than many institutions may be comfortable to do.

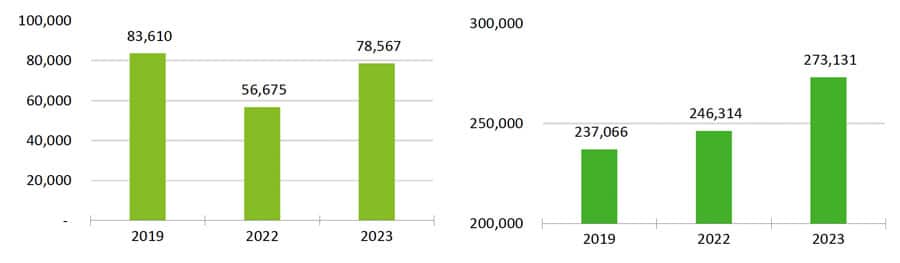

The latest data for Malta’s English Language Teaching (ELT) sector finds that total student weeks for 2023 increased by 15.2% compared to 2019 levels. “This increase in student weeks was due to longer stays during the shoulder months,” explains a recent industry report. “The average length of stay over this period increased from 19.8 days in 2019 to 24.3 days in 2023.”

Total enrolments, meanwhile, continue to dip below pre-COVID levels, with 78,600 student arrivals reported for 2023, a shortfall of just over -6% compared to 2019.

ELT student arrivals (left) and student weeks booked (right) in Malta, 2019–2023. Source: FELTOM/Deloitte

Those are the headline findings from the English Language Travel Industry Report 2023, an annual report produced by Deloitte in collaboration with the industry peak body FELTOM (Federation of English Language Teaching Organizations Malta).

The report also highlights the key role of the ELT sector in Malta’s larger tourism and hospitality industry: “The ELT sector remains an important niche market for the tourism industry in Malta. The sector plays an important role in the diversification strategy of the local tourism sector to promote a more diverse profile of visiting tourists and less reliance on traditional core inbound markets.

During 2023, the sector continued to attract students from markets which are not traditional tourist source markets for Malta, such as Brazil, Japan, and Colombia. Student arrivals from non-EU/EEA countries accounted for 26% of total student arrivals but represented 59% of total student weeks due to the longer training programmes followed by this cohort.”

Overall, sector revenue was also up by 10.9% compared to 2019, driven mainly by increased tuition and accommodation fees.

Speaking at an event to officially launch this year’s findings, FELTOM CEO Jessica Rees-Jones said, “Why does FELTOM produce the report? Why does it matter? It matters because it tells a story. And it matters to the 78,000 and more students that choose Malta in 2023. It matters to the 1,300 [plus] staff in the schools, and how they teach every day…It tells the story of how people make choices of where to study, where to travel, and where to learn.”

Join 37,000 subscribers

and stay up to date on International Recruitment

Cross River Commissioner for Education, Sen. Stephen Odey, has disclosed that he uncovered 1,572 teachers with fake certificate while serving as the Chairman of the State Universal Basic Education Board (SUBEB).

Odey disclosed this on Tuesday in Calabar when the leadership and members of the Nigeria Union of Journalists (NUJ), Cross River Council, paid him a courtesy visit in his office.

The commissioner who served as the chairman of Cross River SUBEB between 2015 and 2022 before he was elected senator in a by-election, said he also discovered many teachers who bought their certificate with as much as N300 thousand.

He said looking at the challenges in the educational sector in the state, he has refused to fold his hand and allow the rot in the system, adding that teachers should be exemplary in everything.

“The rot in the educational system is enormous and we are facing this daunting challenge, that is why we need the support of the media to help in the fight to sanitise the sector.

“I won’t fold my hands to the fact that people are paying money to be appointed principal or head teachers when they don’t even have the capacity or where you give approval for a principal to collect N4,000 and he goes ahead to collect N8,000 from students.

“since I came into office as commissioner and from my days in SUBEB, I have seen a lot because while you are trying to do the right thing people will fight back, however, I am happy that people now know that we are doing the right thing,” he said.

Speaking further, Odey said education was suppose to be the center of excellence in the state because if that sector was affected negatively the state was finished.

He also used the opportunity to debunk claims made earlier in a media report that some states including Cross River had not recruited teachers since 2018, adding that while as chairman of SUBEB in 2019, he recruited 2,500 teachers.

He added that he had written to Gov. Bassey Otu for the approval to recruit 6,000 teachers because the greatest problem affecting teaching and learning in Cross River was inadequate teaching staff.

Earlier, the Chairman of the NUJ, Mrs Archibong Bassey, who commended the doggedness of the commissioner said the media in the state would continue to support him as he strived to sanitise the educational sector in the state.

According to her, “we need to groom our children to be able to compete with the children in other climes.

“I have been following your activities as commissioner and I have seen your passion, even to the point of clamping down on schools that did not meet up with the state’s criteria.”

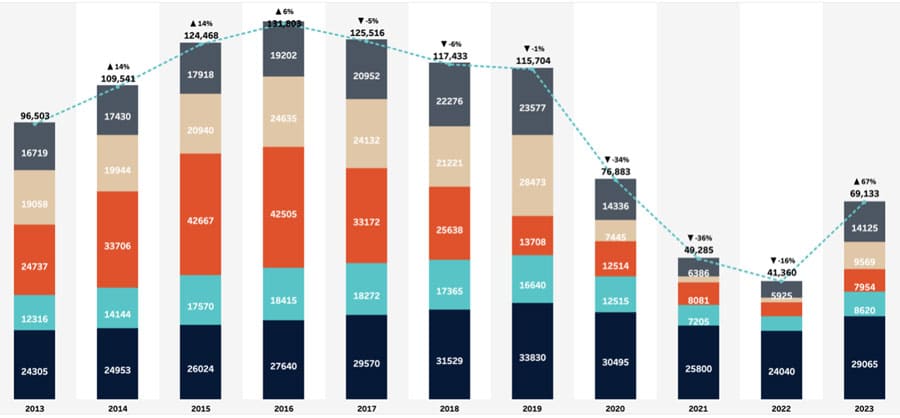

New Zealand’s schools, universities, language institutes, and vocational institutions together hosted 69,135 international students in 2023, a 67% increase in total foreign enrolment over 2022. This represents 60% of the international student base in 2019, when over 115,000 international students were enrolled.

During the pandemic, New Zealand’s borders were closed for longer than any of the other leading English-speaking destinations, fully re-opening only in the summer of 2022. This is part of the reason for the slower recovery of New Zealand’s international student numbers. Another factor is that New Zealand’s international education strategy prioritises balance over limitless growth. The goal is the development of a sustainable sector that brings economic, social, and cultural benefits to the whole country.

Dr Linda Sissons, Acting Chief Executive of Education New Zealand, commented:

“Over 69,000 enrolments from international students all over the world is good news for our education sector and positive for our communities. It confirms that New Zealand is an attractive place to study, offering a quality learning experience inside and outside the classroom in a safe, welcoming environment. New Zealand is a small country and for many students, rubbing shoulders with people from other cultures gives them a greater understanding of the issues facing our complex world. In this time of fragile geopolitics, the melting pot of campus life can help build greater understanding and tolerance.”

The most growth occurred in the university and English-language sectors

The university sector – the largest segment of New Zealand’s overall international education industry – has recovered the most fully of all the sectors, reaching 86% of pre-pandemic volumes for a total of 29,065 students (+21% over 2022). But the English-language sector expanded the most year-over-year, enrolling 9,569 students in 2023 versus only 1,565 in 2022 (+511%), and the schools sector also expanded significantly to 14,125 (+138%).

New Zealand’s Private Training Establishments (PTEs) and Te Pūkenga (New Zealand Institute of Skills and Technology) enrolled 59% and 74% more international students in 2023 than 2022, respectively.

International enrolments in New Zealand, 2013-23. Source: Education New Zealand

Top markets

New Zealand education institutions remain heavily reliant on China (35%) and India (17%), which together make up more than half the total enrolment (52%). This reliance on the top two source markets is similar to Canada and the US (51% and 52%, respectively), but higher than what we see in Australia and the UK, where Chinese and Indian students make up 45% and 41%, respectively, of the total foreign enrolment.

Join 37,000 subscribers

and stay up to date on International Recruitment

After China and India, Japan is New Zealand’s third-largest source market (10%), South Korea is the fourth (5%), and Thailand is the fifth (4%). No other country composes more than 4% of the total foreign enrolment.

Speaking to the issue of diversification, Education New Zealand’s Dr Sissons said:

“Enabling a thriving and globally connected New Zealand through world-class international education is a government priority. We are actively diversifying our recruitment efforts to reach international students in a broad range of countries.”

A just-released global survey report from Intead and Studyportals, Know Your Neighbourhood, contains several surprising findings – including that a substantial segment of international students would be more likely to choose the US over other destinations if Donald Trump were to emerge the victor of the upcoming US election (5 November 2024) and become president for the second time.

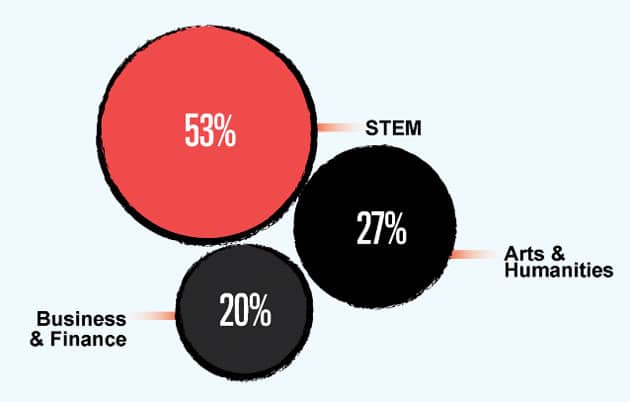

The survey was conducted in March and April of 2024 and drew responses from almost 2,500 students in 106 countries. More than half (58%) were from Africa, 29% were from Asia, and 7% were from Europe; smaller numbers of students were from other regions. Most student respondents were interested in graduate (38%) or postgraduate programmes (37%) – especially programmes oriented in STEM subjects.

More than half of students were interested in STEM, while 27% were exploring Arts & Humanities and 20% were looking at Business & Finance programmes. Source: Intead/Studyportals

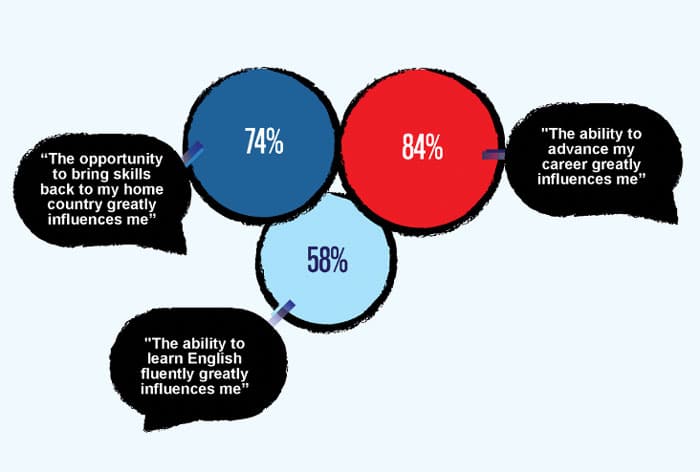

Career motivations a major driver, and many students want to take their skills back home

As usual, career motivations topped the list of reasons for why students were interested in study abroad, and a significant proportion of students were determined to bring skills acquired abroad home to their country. Learning English was also a common theme.

Top motivations for study abroad. Source: Intead/Studyportals

Almost half of students aren’t overly concerned about safety or discrimination

More than 4 in 10 students (44%) globally said they are not influenced by concerns about religious or racial discrimination, personal safety, or political instability when thinking about study abroad. This proportion rose significantly in Latin America, where three-quarters of respondents are unconcerned about discrimination or safety in a host country. More than 6 in 10 Latin Americans also said that safety issues in their own country are not a driver of their desire to study abroad.

Intead/Studyportals researchers offer this hypothesis for the relatively low concern about safety and security:

“Taking into account both of these prompts, these respondents’ generalized indifference may reflect the lifelong navigation of a complex, changeable socio-political environment of the countries’ citizens, which can foster greater desensitization to changeability or alleged lack of security anywhere.

While the percentage of respondents who cited ‘some’ to ‘a lot’ of influence remains high (66% collectively), the lack of reported concern about discrimination among nearly half of our respondents prompts us to reconsider the prevailing narratives surrounding international travel and how safety and acceptance actually impact these young adult travelers. While challenges of acceptance may exist, this substantial percentage of education-seekers are asserting their determination to pursue their academic goals regardless of their concerns about religious/racial discrimination, personal safety, and political instability.”

Join 37,000 subscribers

and stay up to date on International Recruitment

How would a potential Trump presidency affect the US’s appeal as a study destination?

Eight years ago, in the lead-up to the 2016 US presidential election, Intead/Studyportals ran a survey that found (1) a “significant distaste” for then-nominee Donald Trump and (2) a preference for nominee Hilary Clinton. As we know, Trump won that election and during his presidential term (2016–20), he was strikingly committed to ensuring that Chinese and Muslim students felt unwelcome in the US. In 2017, in fact, his administration barred students in six Muslim-majority countries from coming to the US to study.

Under Trump, a trend of declining international enrolments in the US accelerated, and foreign enrolments reached an all-time low in 2020/21. That trend began reversing under President Biden and the number of foreign students in the US reached a near-record high in 2022/23. Recent IDP research has found that the US is now the frontrunner in terms of most-preferred study abroad destinations as policy changes in Australia, Canada, and the UK have diminished those countries’ draw for international students.

International enrolments in the US 2014–23. Source: WES

While campaigning for the 2024 election, Trump has promised that “the most aggressive vetting process in U.S. history” would ensure that only “the most skilled graduates who can make significant contributions to America” will be permitted to remain after they complete their programmes. Needless to say, more restrictive policies would affect the US’s competitiveness in international student markets.

But Trump’s promises of heightened vigilance, and historically distrustful attitude towards immigrants and international students, do not seem to be deterring many prospective international students considering study in the US.

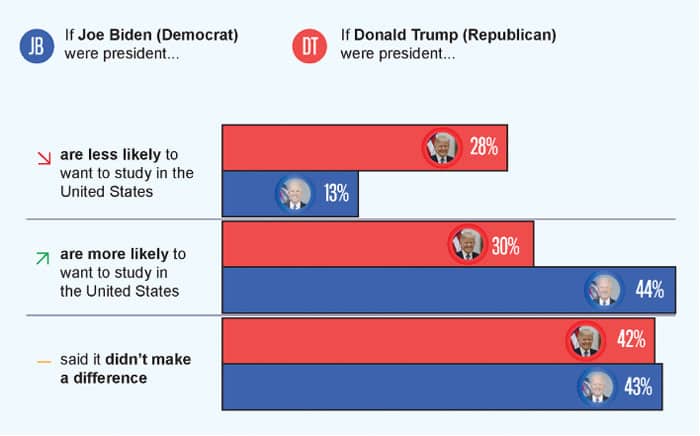

When asked in this year’s survey about their feelings about the upcoming November US election, 44% said that they would be more likely to study in the US if President Biden won – but a sizeable 30% said they would be more likely to do so if Donald Trump won. Moreover, 42% said it wouldn’t make a difference one way or the other which candidate emerged as the victor.

This means that nearly three-quarters of respondents would not be deterred from studying in the US in the event of a second Trump presidency – a far greater proportion than the 28% who said they would be less likely to study in the US should Trump win the November election.

President Biden is preferred over Trump by prospective international students – but not by a wide margin. Source: Intead/Studyportals

Respondents’ relatively mild reaction to a potential Trump victory is especially curious given that the bulk of survey participants came from Africa and Asia – the world regions with the largest number of Muslim-majority countries (and of course, China).

The Intead/Studyportals survey offered respondents an option to write in reasons for their feelings about each presidential nominee. In general, among those who favoured President Biden, the sense was that his presidency would mean “a more traditional diplomatic and international relations approach, potentially fostering a more welcoming environment for international students.”

As for the 30% who would be more likely to want to study in the US under a Trump presidency, written comments indicate that there is a sense that students envision better career prospects under Trump:

“Write-in responses indicate that the economic growth and job creation, along with policies promoting American businesses that may accompany the Republican’s leadership, could increase their career advancement and access to the US job market.”

It bears noting that the US’s gross domestic product (GDP) has increased by 8.4% (when adjusted for inflation) in the four years of President Biden’s administration, higher than the growth rate under former president Trump. But there is a longstanding notion in the US that Republicans (Trump’s party) prioritise the economy more than Democrats (Biden’s party) do, perhaps given Democrats’ more liberal and progressive orientation.

Intead/Studyportals researchers present this astute commentary:

“Additionally, our experience leads us to imagine that Mr. Trump’s America-first rhetoric and policies may appeal to students interested in patriotic ideologies or those seeking a more insular cultural experience. Following our logic further, to these respondents a Trump presidency might also imply that the US will be less involved in foreign affairs, and less inclined to intervene in other countries’ internal issues—a somewhat anti-imperial stance that could appeal to citizens of emerging/developing countries.”

A lot of students “just don’t care” about the result of the upcoming US election

Nearly half of surveyed students (42%) said that the political environment in the US does not make a difference to their motivation to study in the US. Intead/Studyportals researchers posit a number of theories about this finding, including the idea that the US political climate is such that students can hardly take the election seriously. Instead, they are simply focusing on the quality of US institutions and the desire for a good career.

Are students becoming desensitised to political volatility in the US (and elsewhere)?

The Know Your Neighbourhood report includes the following striking graphic. Keep in mind that in 2016, the attack on the US Capitol Building (6 January 2021) by a mob of pro-Trump supporters unwilling to accept President Biden’s electoral victory had not yet occurred. Nor had dozens of criminal charges and convictions against Trump yet proceeded through the courts. Still, student-respondents were twice as likely to say they would want to study in the US under Trump In 2024 as in 2016.

Percentages of students saying they would be more likely to want to study in the US under a Trump presidency – 2016 versus 2024. Source: Intead/Studyportals

The significantly larger proportion indicating increased interest in 2024 under Trump is in many ways astounding, especially given how Trump has approached the issue of international students in the past. But perhaps the finding can be viewed in a context of increasing youth apathy and/or cynicism about politics and politicians in general, as young people watch their world increasingly gripped by extreme weather and devastating wars. As the US heads toward the November election:

The Pew Research Centre has found that 3 in 10 people in 24 countries are in favour of authoritarian political systems – and this proportion rises in Asia and Africa. The poorer people are, the more likely they are to prefer authoritarian governments to democratically elected ones.

China and Russia, both run by ever-more controlling authoritarian regimes, are becoming more powerful around the world, and democratic countries in close proximity are feeling the pressure.

India’s democratic conventions have been challenged under President Modi.

Cuba, Nicaragua, and Venezuela are run by dictators.

Türkiye’s President Erdoğan and Hungary’s President Orbán routinely block EU legislation, and democratic traditions in Türkiye and Hungary have eroded in recent years under those leaders.

Marine Le Pen’s far-right party is gaining ground in France.

Only 12% of African countries are considered truly democratic.

Prospective students are living in an era where the idea of democracy is increasingly under pressure around the world. Amid this context, the idea that a US president who has promised to be “only a dictator on Day 1” may be sworn in on 5 November 2024 is not as shocking as it might once have been.

In the meantime, students still want to study in institutions that can give them the brightest future possible, and that overarching drive may be behind some of the more surprising findings of the Intead/Studyportals research.