It all seemed to happen quite suddenly, and then relentlessly. Beginning in mid 2023 and stretching through 2024, several national governments – notably those in the UK, Australia, and Canada – tightened immigration settings, increased scrutiny of education providers and agents, and made it more difficult for foreign students to obtain visas. In the Netherlands, universities committed to reducing international student volumes to avoid imminent legislative intervention.

We came to expect an announcement every week or two – whether it was news of an immediate cap on new study permits, a massive visa application fee increase, higher financial requirements for students, amendments to work rights, or the withdrawal of most dependants’ permission to accompany students.

The question is: why? Why would governments act to stem the flow of bright international students capable of alleviating critical skills shortages and declining economic productivity? What ended a post-pandemic enthusiasm for welcoming record-high numbers of foreign students?

The answer lies in declining public support for immigration amidst persistent economic pressures and a global migration crisis that is overwhelming critical infrastructure such as healthcare systems and housing.

A quick shift in priorities

The more restrictive policies signal that the cultural and economic value of international students is now secondary to an urgent new priority for elected governments in many advanced economies: reducing migration at seemingly any cost.

Among policy makers, there appears to be little memory of – or concern about – the devastating toll of plummeting international student numbers during the COVID-19 pandemic. Interrupted student mobility flows when borders were closed impacted not only the revenues and staff of education providers, but also the fortunes of whole communities and other business sectors.

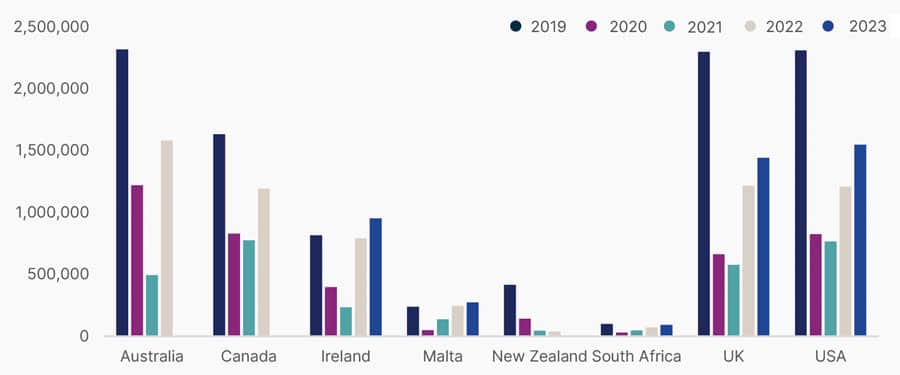

When borders reopened, governments enacted all manner of policies to attract new international students, knowing full well that billions of dollars would return to their economies as a result. Foreign enrolments quickly surged to record-high levels in Australia (nearly 800,000 in 2023), Canada (over 1 million in 2023), and the UK (nearly 700,000 in higher education alone in 2021/22).

But in tandem with these new peaks, more and more stories appeared in national media outlets about a disturbing trend: growing numbers of people in major cities in Australia, Canada, the UK, and elsewhere are struggling to access affordable housing and other vital services, including healthcare. And all this amidst a backdrop of surging inflation, rising costs of living, and economic uncertainty.

These factors combined for a potent political cocktail that has made immigration a hot-button electoral issue in leading study abroad destinations. For example, in Canada, 50% of Canadians responding to a survey conducted by Leger in February 2024 said that “there are too many new immigrants in Canada” — a proportion that more than doubled over January 2023. This stands in sharp contrast to a long-standing belief in previous decades among most Canadians that immigration is a public good.

A global crisis of movement

The world is facing what some have termed a global migration crisis, characterised by historically high numbers of people attempting to cross borders in search of safety and opportunity. The crisis stems from a horrible combination of wars, natural disasters, and crumbling economies. Any or all of these elements are present in dozens of countries, especially in the Global South (a designation generally understood to contain large swaths of Africa, Latin America, and Asia). Millions of people in affected regions face difficult or unsafe circumstances, and so many are driven to seek temporary or permanent settlement elsewhere.

UNESCO figures indicate that there were 281 million international migrants as of 2020 (the latest year for which global data has been compiled). Of that total, 169 million were labour migrants and 117 million were displaced people (mostly asylum and refugee claimants).

International students, who fall under the category of “temporary migrants,” currently number about 8 million worldwide. This segment is a drop in the bucket, even a rounding error, when you consider the total migrant population of over 280 million people. But international students are nevertheless caught up in the same migration politics. They are explicitly counted in net migration figures in the UK, for example, and in temporary migration figures in Canada.

What is to be done?

There is little debate about the following facts:

- Rising numbers of people moving from country to country do place pressure on local services, labour markets, and housing markets.

- There remains an undersupply of housing and healthcare services – and persistent concerns about rising costs of living – in many top destinations for international students.

- Growing segments of the public in those countries want to see immigration levels reduced. This has fuelled not only the rise of ultra-nationalist and/or far-right movements, but also more restrictive immigration policies in liberal democracies such as Australia, Canada, and the UK.

- What is sometimes known as the “social licence” afforded to the international education sector has been eroded due to shifts in public support for immigration, media coverage of unethical practices on the part of a small segment of education providers and agents, and a perception in some circles that the sector is more concerned with revenues than with the well-being of international students.

Across our industry, we all have a role to play in restoring the standing of international education in the eyes of government and the public. The way forward includes a renewed commitment to providing an outstanding study experience to all students: in the classroom, through student services, by securing more and better accommodation, and by improving graduate outcomes.

It will be crucial to:

- Build stronger links between recruitment and housing availability;

- Align recruitment with labour market needs;

- Work in collaboration with industry and other stakeholders to ensure improved career outcomes for international students, both in their study destinations and at home;

- Improve communications with government stakeholders and the public at large;

- Advocate for international student numbers to be tracked separately from net migration figures.

This has been a year in which global political and economic pressures have had a profound impact on international student mobility. Among the many important lessons to be drawn from 2024 is how vulnerable our sector can be to changes in policy and how critical it is to communicate the benefits and standards of international education to policy makers and other key stakeholders.

For additional background, please see:

- Join the ICEF Monitor Global Summit (23 September 23 2024, London). A landmark one-day summit bringing together the industry’s senior leaders, policy makers, and experts, all focused on shaping the future of the international education sector.

Source